- +91 9623131787

-

How many times have you encountered the quote "Health is Wealth"? Probably many times.

Though we all know our health should be our top priority, we often ignore it. We know good health comes from healthy eating, routine exercise, health check-ups, etc. But why do we ignore health insurance?

Health insurance shouldn't be ignored if you don't wish to worry about arranging finances during medical treatments. With rising medical costs, taking a policy to cover such expenses has become a necessity.

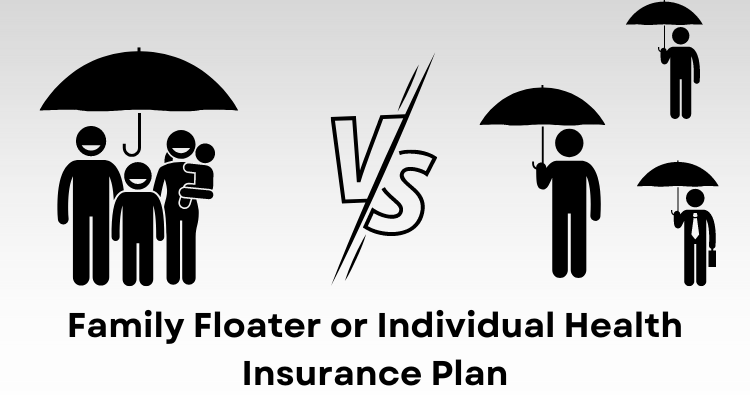

While getting a health insurance plan, you must choose between opting for an individual or a family plan.

In this blog, we'll cover some significant differences between the two to help you make a wise decision.

Individual health insurance focuses on one person. It provides coverage to one person only. Neither the premium paid nor the sum insured can be shared with someone else.

Family floater insurance covers all family members in a single plan. This means that both the insurance premium paid and the sum insured can be shared among many family members.

The coverage in the case of individual health insurance plans is provided to the policyholder who pays the premium. Let's say you have taken health insurance for Rs. 5 lakhs. Then the health insurance company will compensate the hospital bills for your treatment only.

All family members are covered under a single plan in a family health insurance plan. For example, you opted for an insurance policy for Rs 5 lakhs for yourself, your spouse, and one child. Then your whole family members will have to share the sum insured, i.e. Rs. 5 lakhs.

An individual health insurance plan is suitable for individuals with specific health needs. It is best suited for senior citizens.

However, a family plan may be suitable for couples or nuclear families with no senior citizens. It is because a hefty premium is charged for senior citizens, and they need an individual policy for their specific needs.

The major advantage of choosing an individual plan is getting a specific sum insured only for your personal needs. Also, you can claim maximum coverage of your risks.

The major advantage of family floater plans is that the premium is more affordable than that of an individual one. It saves from taking too many individual policies.

Lack of flexibility and high individual premiums are a few of the limitations of individual health insurance plans.

And family floater plans suffer from drawbacks like insufficient sum insured to effectively cover all the members of the family. Also, there is a higher probability of raising a claim under such plans. As a result, you won't be able to experience a no-claim bonus. In simple words, if any of your family members claims during a year, no claim bonus would not be applicable.

Also, if your children reach a certain stage (18-25 years, depending on the type of policy), they won't be covered in a family health insurance plan.

No single policy is perfect for all individuals or families. Many factors affect your choice besides the premium to be paid and the risk covered.

But if you can afford to take individual health insurance policies, you must go for them. These policies not only ensure that your specific health needs are met but also benefit you from a no-claim bonus. NCB means you would have more coverage or pay fewer premiums if you don't claim benefits during a policy year.

But if you don't have a medical history of severe health conditions, can't pay huge premiums, or don't have a senior citizen in the family, family plans would work for you.

No one policy is best for everyone. Whether you take an individual or family health insurance plan, make sure to check its pros and cons.

Also, do consider factors like health conditions/risk, family members, age, coverage of the policy, etc., before purchasing a policy.

Any policy that caters to your needs is best for you. Nevertheless, don't forget to take a health insurance policy at any cost.

This blog is purely for educational purposes and not to be treated as personal advice. Insurance is the subject matter of solicitation.

After gathering more than 12 years of experience in the Mutual Fund &Finance industry, Yogesh Bhave &Janhavi Bhave decided to set to start Surabhi Wealth LLP in the year 2017.

SURABHI WEALTH LLP

587 Shaniwar Peth,

Near Narayan Peth Policy Chowky,

Pune - 411030

+91 9623131787

Copyright © Surabhi Wealth LLP. All rights reserved.

.png)